COVID-19 created a tough economic environment and the government made changes to allow small businesses to to restructure debt more easily and with less expense.

What are the benefits of small business restructuring?

Small business restructuring was introduced for small businesses, its creditors, and its employees to get the benefits of:

- reduced costs

- shortened turnaround times

- increased and easier access

- retained control by business owners/directors (through the debtor-in-possession model).

Who can access small business restructuring?

Currently incorporated companies with liabilities with less than $1 million (excluding employee entitlements) are eligible. All tax lodgments must be up to date. This means that directors have lodged any returns, notices, statements, applications, or other documents as required by taxation laws (within the meaning of the Income Tax Assessment Act 1997).

Under the restructuring plan process, all employee entitlements that are due and payable must be paid before that plan can be put to creditors. And requires directors to make a declaration about certain company transactions and what their reasonable grounds are for believing they qualify for a restructuring plan.

The small business restructuring process can only be used once in a seven-year period. This applies to both the company and the directors (including former directors who resigned in the previous 12 months). It also is excluded if both the company and directors entered into a small business restructure appointment or simplified liquidation (which was introduced with the restructuring process reform) in the same seven-year period.

Why would directors choose to use restructuring?

Directors who want to try to save their business through restructuring company debt while retaining control of business operations and creditor relationships.

Is restructuring available to me?

Companies are expected to be the primary user of restructuring; however, it is available to other incorporated entities such as registered clubs, co-operatives etc. Sole traders do not have an equivalent option under the personal insolvency regime (although a part 10 agreement under Part X of the Bankruptcy Act 1966 may produce a similar outcome in some cases).

Directors must also resolve that the company is insolvent or is likely to become insolvent at some future time and that a restructuring practitioner should be appointed.

Liabilities for the purposes of restructuring includes debts to related parties and includes contingent liabilities.

What do directors need to declare?

Within five business days after the restructuring begins (or longer if approved by the restructuring practitioner), directors must provide the restructuring practitioner with a signed declaration stating that:

- The company is eligible.

- Whether the company has entered into a voidable transaction.

- The directors believe on reasonable grounds that the company meets the eligibility criteria, and why.

Transactions outside the ordinary course of business, such as material asset transfers and forgiving related party debts, are the sorts of transactions that might be voidable in a liquidation. If in doubt, directors may require appropriate advice before making the declaration.

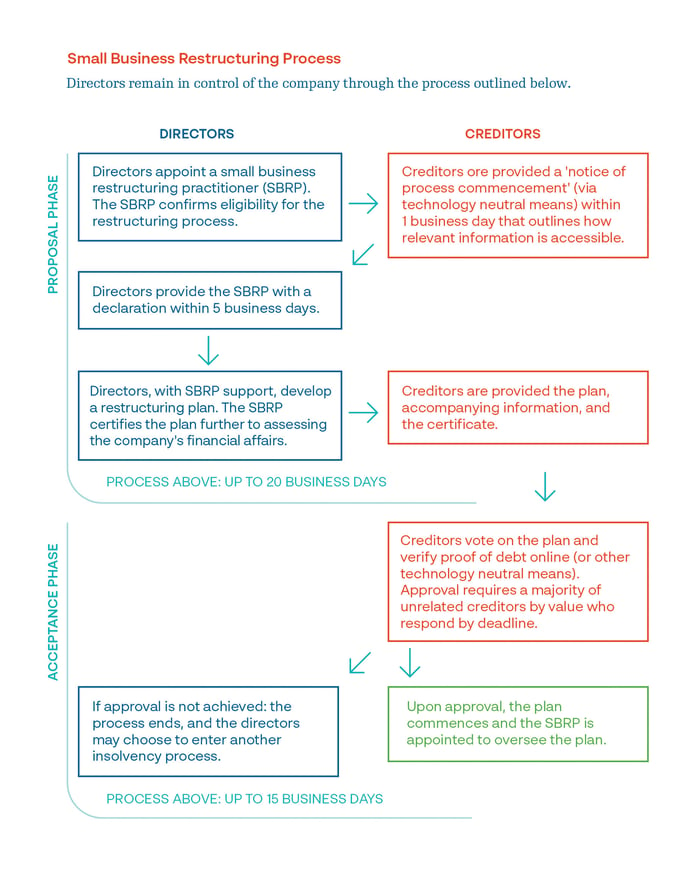

How does the restructuring process work?

Directors can continue to trade in their company’s normal course of business (subject to certain control and restrictions) while undergoing the restructuring process.

The process can take up to 35 business days and is broken down into two phases:

- The proposal phase: Directors and external practitioner work on plan for up to 20 business days.

- The acceptance phase: Creditors have up to 15 business days to vote thereby approving or rejecting the plan.

The flowchart below outlines the steps involved.

A plan is approved when a majority in value of voting creditors vote in favour, however related creditors are excluded from voting. A range of conditions apply to how the restructuring plan is “effectuated” and terminated following any contraventions.

A plan is approved when a majority in value of voting creditors vote in favour, however related creditors are excluded from voting. A range of conditions apply to how the restructuring plan is “effectuated” and terminated following any contraventions.

Are there restrictions on the plan directors can put forward?

All restructuring plans must include several prescribed terms and conditions. For example, admissible debts and claims must rank equally and receive a pro-rata share of the funds available for distribution (including related creditors). Additionally, a creditor cannot receive a transfer of property other than money.

The restructuring plan can be conditional on a future event occurring e.g. a sale of property/asset within a maximum of 10 days after creditors accept the plan.

The restructuring plan is limited to a three-year term.

How are secured creditors impacted?

Secured creditors are subject to similar moratorium provisions as applies in a voluntary administration and will only be bound by a restructuring plan to the extent they agree to be bound, under regulation 5.3B.29. However, any shortfall a secured creditor sustains will be covered by the restructuring plan and again they are bound by it.

How are related creditors impacted?

Related creditors do not get to vote on the plan. However, they receive a distribution under the restructuring plan.

How does an approved restructuring plan become complete?

When an approved restructuring plan is fully effectuated in accordance with its terms, it terminates (is completed), and the company is freed from the debts covered by the plan.

Can an approved restructuring plan be terminated?

Yes. A plan can be terminated if:

- A creditor obtains a court order.

- If the plan is conditional on a particular event occurring within 10 business days after the plan is made, and the event does not occur within that period (i.e. a condition precedent).

- If there is a breach that goes un-remedied for 30 business days.

- If an administrator, liquidator or provisional liquidator is appointed to the company.

Can an approved restructuring plan be varied later?

Yes. However, varying an approved restructuring plan might not be commercially viable in many cases as a court order is required.

What does the restructuring practitioner do?

All registered liquidators are automatically entitled to act and be appointed as a restructuring practitioner. Only registered liquidators can act and be appointed to the new simplified liquidation process.

The restructuring practitioner’s role includes:

- helping determine eligibility

- supporting the directors to develop its plan and review the company’s financial affairs

- certifying the plan for creditors to vote on

- managing disbursements if plan is approved.

Directors stay in control of the company’s day-to-day activities, therefore the restructuring practitioner is not personally liable for the company debts/actions.

What does a small business restructuring plan cost?

The basis for the restructuring practitioner’s remuneration is:

- A fixed fee for the proposal phase, which directors resolve prior to the appointment.

- A fixed percentage of the recoveries from the plan, which creditors approve.

The fixed fee covers the following duties:

- helping determine eligibility

- supporting the company to develop its plan and review its financial affairs

- certifying the plan for creditors to vote on.

Referral fees are prohibited in all other types of formal insolvency; however, they are impliedly permitted by regulation 5.3B.16.

How should a company under a restructuring plan be referred to?

A company subject to the restructuring process must advertise this status. For example, ABC Pty Ltd should be described on all public documents as “ABC Pty Ltd (restructuring practitioner appointed)”.

Last updated: 11 01 24